")

Saudi Aramco is looking to sell 0.5 per cent of its shares to private investors – Saudi nationals, qualifying resident expatriates, and GCC citizens – as part of the record breaking initial public offering of shares in the most profitable company in history.

The percentage allotted to private shareholders was officially confirmed for the first time in the formal prospectus for the share offer on the Tadawul stock exchange, along with a wealth of information about the world’s biggest oil company.

With 200 billion Aramco shares current owned by the government, the amount targeted towards private shareholders would be 1bn shares.

The 658-page document was filed on the website of the Capital Markets Authority (CMA) – the Saudi regulator – late on Saturday night, following approval by the CMA for the IPO last week.

It still lacks crucial information on the sale – like the total percentage of the company to be sold, the level at which the shares will be priced, and an estimate of the total value OF Aramco.

But the prospectus will be pored over by private investors and foreign investing institutions as they weigh up whether to invest in the most profitable company in the world - and how much of their funds to allocate to the IPO.

If the IPO goes ahead at previously indicated levels, it could easily beat the previous record share sale, the $25bn offering of stock in Alibaba on the New York Stock Exchange.

Aramco executives, bankers and other investment advisers will now embark on a whirlwind tour of Saudi, Gulf and international investors to gauge support for the IPO – a process known as “bookbuilding” – after which the final financial aspects of the offer will be determined.

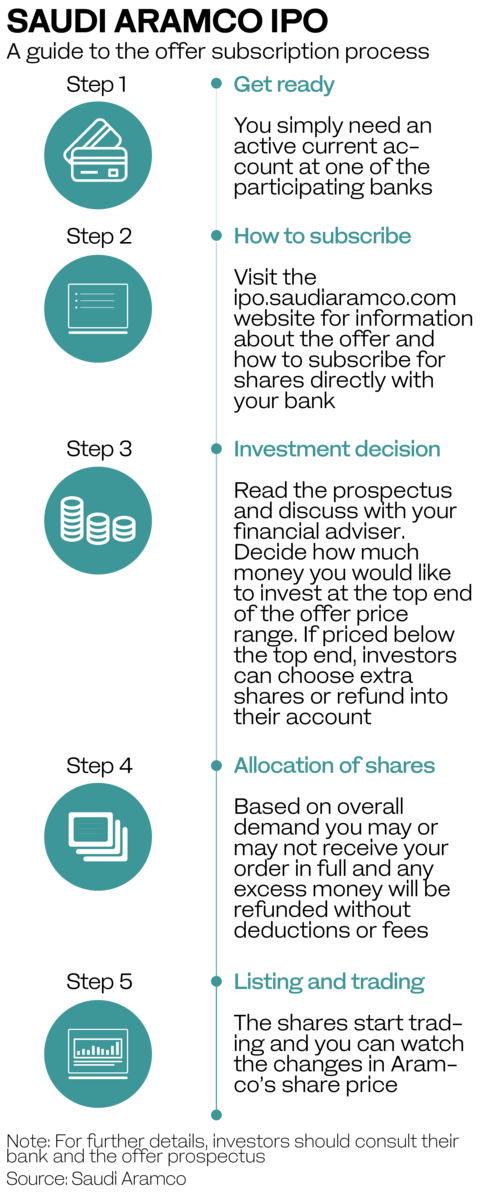

Bookbuilding starts for both tranches of investors on Nov. 17, and end on Nov. 28 for individual investors, and on Dec. 4 for investing institutions.

Private investors who buy shares in the IPO, and who hold them for a period of six month after trading begins in December, will receive bonus shares up to a total of 100 shares, the prospectus confirmed.

The government of Saudi Arabia, which current owns the shares, has undertaken to sell no more for a six-month period after trading begins, nor can Aramco issue more shares in that period.

Although the IPO at this stage is a Tadawul-only launch, the government has said that in the future it could consider selling further shares on a foreign stock exchange.

The prospectus also recognizes “foreign strategic investors” as a source of potential demand for the IPO, opening up the possibility that big foreign wealth funds in Asia or elsewhere may want to get involved in the offering. There has been speculation that Chinese financial groups could be interested, as well as sovereign wealth funds in other GCC countries.

The prospectus also contains detailed information on Aramco’s estimates of demand growth for its key crude product, as well as data on the Kingdom’s oil reserves, refining capacity and governance procedures.

As is standard in all share prospectuses, there is also a detailed analysis of the risks involved in investing in the shares.