")

The week that was:

Global COVID-19 cases surpassed 60 million.

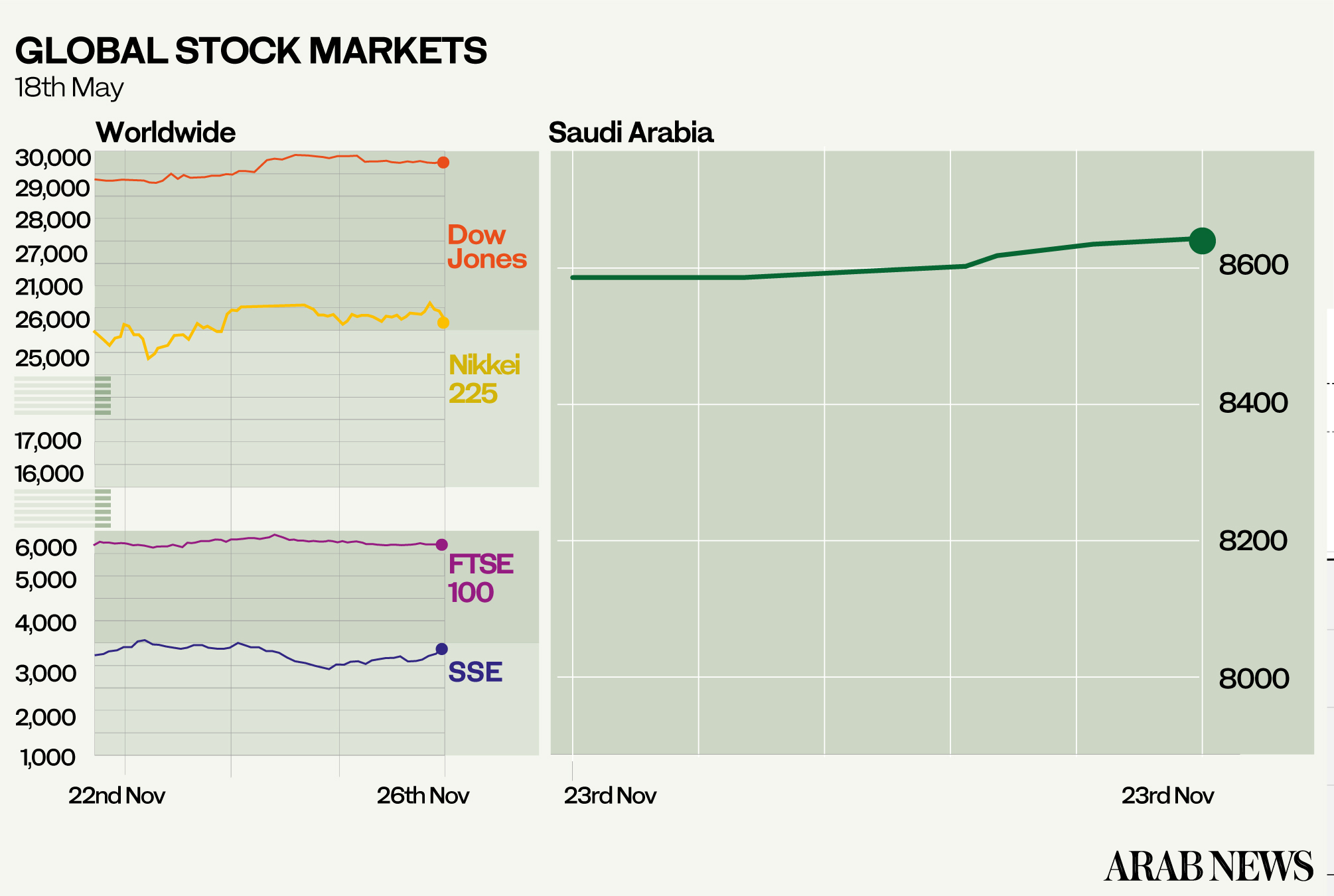

Equity markets soared on positive vaccine news. On Wednesday the Dow Jones reached an all-time high, topping 30,000. The dollar dropped to a two-and-a-half-year low reflecting the risk-on sentiment.

The AstraZeneca / Oxford vaccine trial is marred by controversy over trial size and methodology. The company plans to address concerns with a possible additional global trial.

Developed markets have bought 95 percent of the Pfizer/BioNTech and Moderna vaccines. More than 40 percent of the AstraZeneca vaccines have so far been earmarked for low- and middle-income countries.

US first-time jobless seekers came in at 778,000 for the week ending Nov. 21 — up by 30,000 compared to the preceding week, which marked the second weekly increase. Seasonal incomes fell by 0.7 percent in October and spending increased by 0.5 percent. Going forward, incomes are bound to decline further, because about 12 million people will be affected when two pandemic benefit programs expire at the end of December.

President-elect Joe Biden nominated Janet Yellen as secretary of the treasury, which was well received by the market.

The eurozone composite PMI fell to 45.1 in November from 50 in October. (A PMI below 50 reflects economic contraction.) The ECB governing council fears widespread business closures as restrictions and lockdowns affect business. Travel retail and hospitality are particularly affected.

In the same vein, German Chancellor Angela Merkel requested all ski resorts in Europe to remain closed for the time being, which would be hard for smaller Alpine nations, where the ski sector is a major economic contributor. In Austria, for example, ski resorts contribute 4 percent to GDP and account for nearly 8 percent of employment during the winter months.

The UK will borrow £394 billion, the biggest amount in peacetime. Chancellor of the Exchequer Rishi Sunak still needs to find an additional £27 billion to balance the budget. In 2021 unemployment is expected to reach 7.5 percent or 2.6 million, reflecting the worst downturn in 300 years. By 2025 the economy will be 3 percent lower than expected in March.

China’s industrial profits are up 28.8 percent, a further indication that the economic recovery is stabilising. Copper and aluminum advanced further on the news. Copper is up about 50 percent since March.

The China-Australia trade frictions went beyond coal, barley and wheat, as the country accuses Australian winemakers of dumping. Importers are required to provide temporary deposits between 107-112 percent until the anti-dumping probe is concluded. China represents a $900 million market for Australian wine growers and the Middle Kingdom is also Australia’s biggest export market.

The UAE will allow 100 percent foreign share ownership in companies as of Dec. 1. UAE GDP is expected to contract by 6.6 percent in 2020 and the move is designed to boost growth. It comes on the heels of giving 10-year visas for foreigners, who account for 80 percent of the country’s population.

Sabadell discontinued acquisition talks with BBVA, because they could not agree on price. This puts a spanner in the works of the overdue banking consolidation in Spain. Sabadell’s shares dropped 18 percent on the announcement.

Focus:

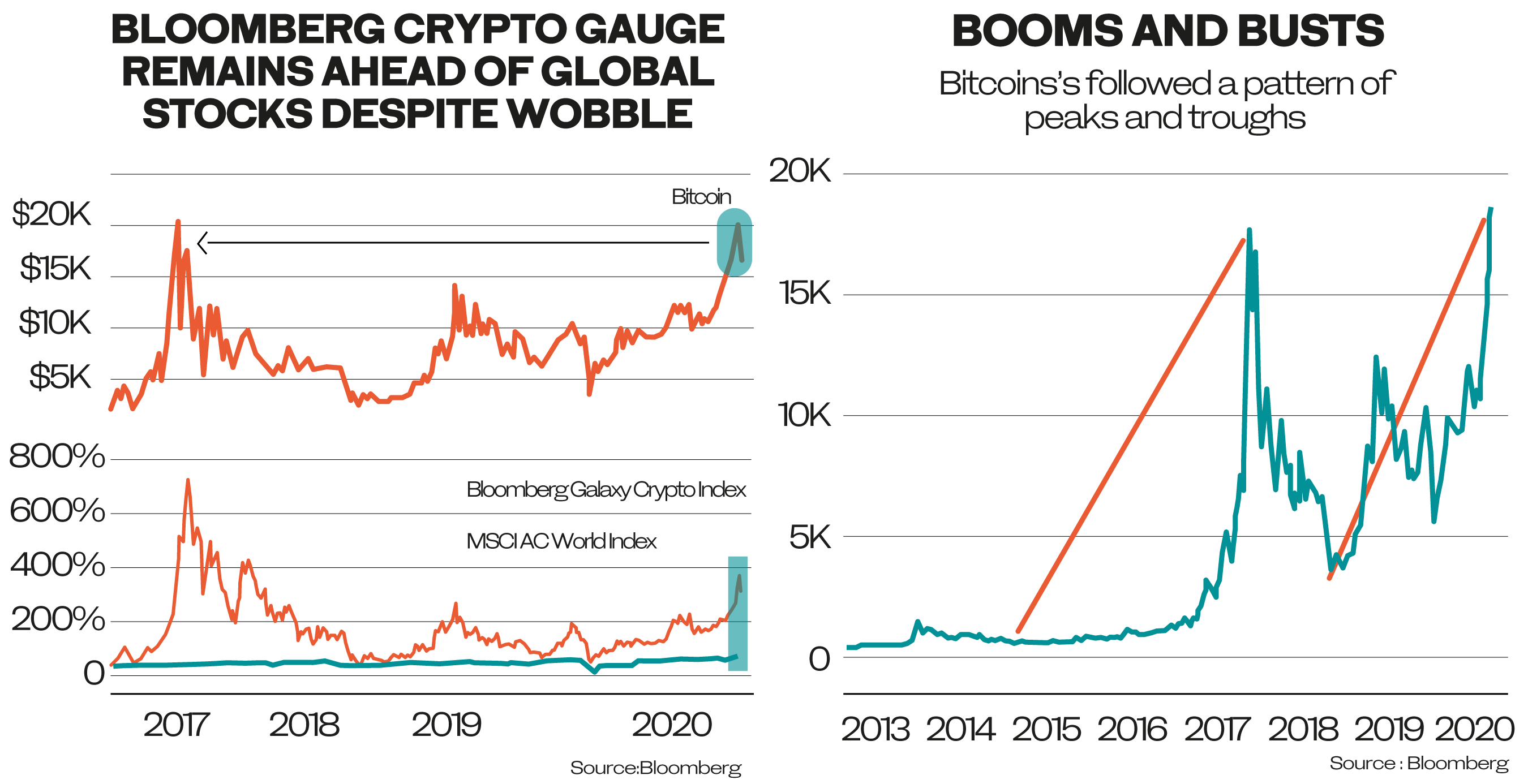

Bitcoin saw a 14 percent drop on Thursday after coming within $7 of its all-time high. Bitcoin rose about 50 percent over the past three months and 140 percent since the beginning of the year. The crypto currency stabilized into Friday.

This highlights the question whether cryptocurrencies can serve as a store of value, given their historically wide swings between sell-offs and rallies.

We should probably not compare the current sell-off to 2017, because the rise of cryptocurrencies was in part a reaction to monetary easing programs by central banks.

This particular rout was influenced by rumors that the US government envisaged new regulations to put an end to anonymous ownership in digital currencies.

Cryptocurrencies have generally been in the purview of retail investors. Big institutions such as JP Morgan or Fidelity have only just begun to direct funds into the sector in a meaningful way.

Cryptocurrencies are dominated by “whales” (large-scale anonymous investors): According to Flipside Crypto, about 2 percent of anonymous ownership can be tracked to 95 percent of ownership on the blockchain. This has big ramifications on value and volatility when whales liquidate positions.

Where we go from here:

Black Friday brings trouble to Amazon in Europe as unions and employees threaten to go on strike, protesting over sick pay, pandemic safety and a raft of other grievances.

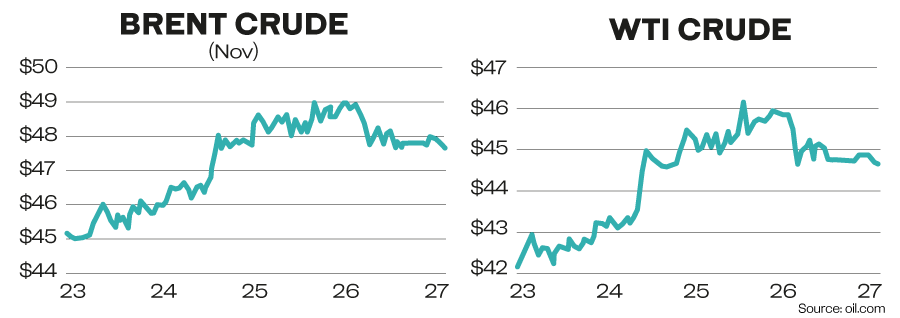

OPEC+ ministers have scheduled a meeting on Nov. 30 / Dec. 1. The recent oil rally, which was based on vaccine hopes, has abated slightly. However, it renders what was already a tricky meeting more difficult. Non-OECD stocks are still way above their 5-year average, anaemic demand in North America and Europe and an extra 1 million bpd out of Libya render the planned reduction of supply cuts from 7.7 million bpd to 5.8 million bpd difficult. An extension of cuts at current levels was under consideration, but the higher oil prices will make it difficult to convince several members of the necessity to leave cuts at current levels. The UAE is said to review membership and Nigeria and Iraq feel that country-specific considerations need to be given greater consideration when setting and monitoring cuts. If the organization decides to reduce cuts according to schedule, an extra 3 million bpd (2 million from OPEC+ cut reduction plus 1 million from Libya, which is exempt from cuts) would hit markets as of January.

Brexit negotiations will continue face-to-face over the weekend. Informed sources are optimistic that an agreement can be struck, bringing the likelihood of a deal to 80 percent. This should not obfuscate the fact that any agreement, which has already been priced-in by markets, is very light, leaving out important parts of the economy such as the services sector.

Poland and Hungary vowed to continue blocking the EU’s seven-year budget and pandemic rescue package, objecting to tying stimulus money to rule-of-law criteria.

— Cornelia Meyer is a Ph.D.-level economist with 30 years of experience in investment banking and industry. She is chairperson and CEO of business consultancy Meyer Resources. Twitter: @MeyerResources